EN version

As Treasurer, I try to educate our members both about financial terminology and about sound financial management. In this installment of “Exploring the Language of Finance,” we focus on debt management. In fact, Esperanto-USA is very fortunate: we do not have large debts that we need to pay off. Unlike many other nonprofit organizations, we have meaningful investment accounts that we use to carry out our mission – to educate in and about Esperanto in the United States.

But to understand good financial management, we have to know how to use debt, when it might make sense to take on debt to move our programs forward, and how to manage that debt so that we pay it off properly and according to a plan. That phrase “according to a plan” is important: the way we pay off debts depends on several factors, including the interest rate and the organization’s overall strategy. In this article, we’ll focus mainly on that strategy.

We’ll introduce two new financial concepts, both related to repaying debt: the debt avalanche method and the debt snowball method. In the avalanche method, you pay off debts in order of their interest rate (from the highest to the lowest). In the snowball method, you pay off debts in order of their outstanding balance (from the smallest to the largest). The avalanche method prioritizes interest rates in order to minimize the amount of interest the organization will pay over time. The snowball method prioritizes the speed of closing out individual debts so that we can clearly show our members that we are actively managing our obligations.

Here’s an infographic which will hopefully be useful to see the differences:

Now let’s look at a short example dialog between a board member and the treasurer about debt management.

Sofia: Mateo, in your reports you sometimes mention our debts, even though they’re relatively small. How do you decide which ones to pay off first?

Mateo: I always start with the important numbers. For each debt, I note the interest rate, the principal, and the current outstanding balance. Only after that can we choose a good repayment plan.

Sofia: And where do the two methods you just mentioned – the debt avalanche method and the debt snowball method – come in?

Mateo: In the debt avalanche method, we sort our debts by interest rate, from the highest to the lowest, and direct every extra dollar toward the debt with the highest rate. That minimizes the total interest we pay over time.

Sofia: So that’s the “mathematically best” one?

Mateo: From a pure interest-cost point of view, yes. But it isn’t always the most motivating for people. The debt snowball method works differently: we sort debts by outstanding balance, from the smallest to the largest. We pay off the smallest debt first so we can see quick, concrete progress.

Sofia: That seems helpful when communicating with members: “Here’s a debt we’ve already eliminated.”

Mateo: Exactly! Sometimes an organization chooses a mix: it defines a repayment plan that mostly follows the avalanche method, but leaves room for one or two “quick wins” using the snowball method.

Sofia: And where does our emergency fund fit into all of this? Should we use it to pay off debts faster?

Mateo: Only up to a point. I’d like Esperanto-USA to always maintain a basic emergency fund for unexpected costs. Anything above that level can indeed be used to pay down debt, but without risking that one surprise expense throws us right back into new debt.

Sofia: It sounds like having a good debt strategy is just one piece of a bigger picture and good financial management.

Mateo: That’s right. If we keep planning this way, our long-term goal is greater financial independence for the organization: enough income and reserves to support our programs without relying too heavily on taking on new debt.

Why does this little scene matter?

In this short conversation, the Treasurer shows that “paying off debt” is not just a technical step, but part of a broader strategy. The board member learns that:

- it’s important to look at interest rates, principal, and outstanding balances, not just the total amount of debt

- different repayment strategies – the debt avalanche method and the debt snowball method – offer different advantages (financial efficiency vs. psychological motivation;

- a clear repayment plan and a solid emergency fund help protect the organization from financial shocks

- the long-term goal is greater financial independence, so the association can choose its projects based on mission, not on its debts

This reflects the real work of Esperanto-USA and, at the same time, gives members vocabulary they can use to think more clearly about their own personal finances.

New and key terms

| Esperanto term | English term | Explanation |

|---|---|---|

| ŝuldo | debt | Money that must be repaid to a lender. |

| kvitigi (ŝuldon) | to pay off / to settle | To repay a debt in full so that it is no longer outstanding. |

| interezprocento | interest rate | The percentage cost of a loan or the percentage return on an investment. |

| ĉefsumo | principal | The base amount of a loan or debt, without interest. |

| ŝuldsaldo | outstanding balance | The remaining portion of a debt that still needs to be repaid. |

| pagplano | repayment plan | A structured plan for how much and how often payments will be made to reduce debt. |

| avalanĉa metodo | debt avalanche method | A strategy in which extra payments go first to debts with the highest interest rate. |

| neĝbula metodo | debt snowball method | A strategy in which you first pay off the debt with the smallest outstanding balance to gain quick wins. |

| kriz-fonduso | emergency fund | A dedicated savings reserve for unexpected expenses or crises. |

| financa sendependeco | financial independence | A state where income and reserves are sufficient to cover needs without relying on new debt. |

Even though Esperanto-USA does not currently carry heavy debts, it’s important for us – both as a board and as members – to understand how to use debt thoughtfully and how to pay it off according to a plan. Concepts like the debt avalanche method, the debt snowball method, a clear repayment plan, and a healthy emergency fund help protect the organization from future shocks and strengthen our ability to advance our mission.

Kiel kasisto, mi strebas eduki niajn membrojn kaj de financfakvortoj kaj de bona financadministrado. En ĉi tiu numero de “Esplorante la Lingvon de Financoj”, ni fokusiĝas pri administrado de ŝuldoj. Fakte Esperanto-USA estas tre bonŝanca, ĉar ni ne havas grandajn ŝuldojn, kiujn ni devas kvitigi. Malkiel multaj aliaj neprofitcelaj organizaĵoj, ni havas investokontojn, kiujn ni uzas por plenumi nian mision: eduki en kaj pri Esperanto en Usono.

Sed por kompreni bonan financadministradon, oni devas scii kiel uzi ŝuldojn, kiam valoras konsideri pruntojn por antaŭenigi niajn programojn, kaj kiel trakti tiujn ŝuldojn por bone kaj laŭplane kvitigi ilin. Rimarku tiun vorton: “laŭplane”. Fakte la metodo, kiun ni sekvas kvitigi ŝuldojn dependas de pluraj aferoj, ezk. la interezprocentoj kaj strategioj de la organizaĵo. En ĉi tiu artikolo, ni fokusiĝos precipe pri la lasta temo.

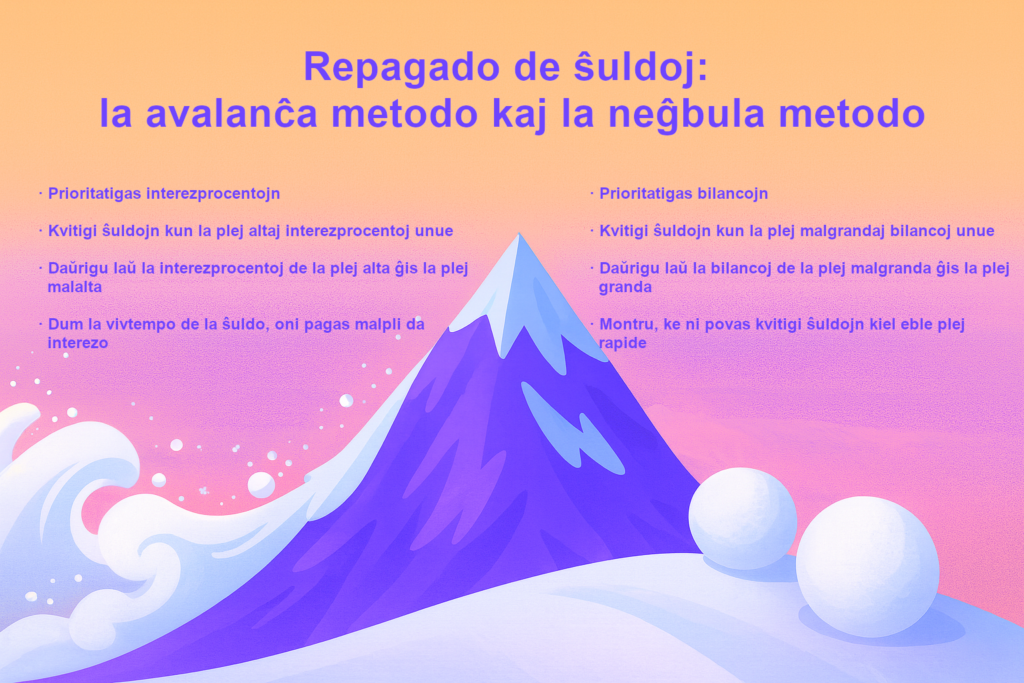

Mi enkondukos du novajn financkonceptojn, kiuj ambaŭ rilatas al repagado de ŝuldoj: la avalanĉa metodo kaj la neĝbula metodo. En la avalanĉa metodo, oni repagas la ŝuldojn laŭ la interezprocentoj (de la plej alta al la plej malalta). En la neĝbula metodo, oni repagas la ŝuldojn laŭ la ŝuldsaldoj (de la plej malgranda ĝis la plej granda). La avalanĉa metodo prioritatigas la interezprocentojn por minimumigi la kvanton de interezo, kiun la organizo pagos. Sed la neĝbula metodo prioritatigas la rapidecon de kvitigo de unuopaj ŝuldoj por ke ni povu montri al niaj membroj, ke ni aktive traktas niajn devojn.

Jen bildo, kiu espereble utilas klarigi la diferencojn:

Nun, ni rigardu mallongan ekzemplan dialogon inter la kasisto kaj alia estrarano pri ŝuldoadministrado.

Sofia: Mateo, en viaj raportoj vi foje mencias niajn ŝuldojn, eĉ se ili estas relative malgrandaj. Kiel vi decidas, kiujn kvitigi unue?

Mateo: Mi ĉiam komencas per la gravaj ciferoj: por ĉiu ŝuldo mi notas la interezprocenton, la restantan ĉefsumon kaj la nunan ŝuldsaldon. Nur post tio eblas elekti bonan pagplanon.

Sofia: Kaj kie eniras la du metodoj, pri kiuj vi ĵus parolis – la avalanĉa metodo kaj la neĝbula metodo?

Mateo: En la avalanĉa metodo ni ordigas la ŝuldojn laŭ interezprocento, de la plej alta ĝis la plej malalta, kaj direktas ĉiun kroman dolaron al la ŝuldo kun la plej alta interezo. Tio minimumigas la interezon, kiun ni pagos longtempe.

Sofia: Do ĝi estas “matematike plej bona”?

Mateo: Plej efika el la vidpunkto de interezo, jes. Sed ne ĉiam plej motiva por homoj. La neĝbula metodo funkcias alimaniere: ni ordigas la ŝuldojn laŭ ŝuldsaldo, de la plej malgranda ĝis la plej granda. Ni unue kvitigas la plej malgrandan ŝuldon, tiel ke ni rapide vidas konkretan progreson.

Sofia: Tio ŝajnas utila por komuniki al membroj: “jen ŝuldo, kiun ni jam fermis”.

Mateo: Ĝuste! Foje organizaĵo elektas kombinaĵon: ĝi difinas pagplanon kiu plejparte sekvas la avalanĉan metodon, sed krome permesas al ni montri unu aŭ du neĝbulajn “rapidajn venkojn”.

Sofia: Kaj kie eniras nia kriz-fonduso? Ĉu ni uzu ĝin por pli rapide kvitigi ŝuldojn?

Mateo: Nur parte. Mi ŝatus, ke Esperanto-USA ĉiam havu bazan kriz-fonduson por neplanitaj kostoj. Super tiu nivelo ni ja povas uzi plian monon por ŝuldoj, sed sen riski, ke unu subita elspezo nin reĵetas en novan ŝuldon.

Sofia: Ŝajnas, ke bona strategio pri ŝuldoj estas parto de pli granda bildo pri bona financadministrado.

Mateo: Jes. Se ni daŭre planas tiel, nia longtempa celo estas pli granda financa sendependeco por la organizaĵo: sufiĉaj enspezoj kaj rezervoj por subteni niajn programojn, sen tro fidi je ajna nova ŝuldo.

Kial tiu sceneto gravas?

En la dialogo la Kasisto montras, ke “kvitigi ŝuldojn” ne estas nur unu teknika paŝo, sed parto de pli vasta strategio. La estrarano lernis, ke:

- necesas rigardi interezprocentojn, ĉefsumojn kaj ŝuldsaldojn, ne nur la sumon de ŝuldoj

- ekzistas malsamaj repagstrategioj – avalanĉa metodo kaj neĝbula metodo – kun malsamaj avantaĝoj (financa efikeco kontraŭ psikologia instigo)

- klara pagplano kaj sana kriz-fonduso protektas la organizaĵon kontraŭ ŝokoj

- la fina celo estas pli granda financa sendependeco, tiel ke la asocio povas elekti projektojn laŭ sia misio, ne laŭ siaj ŝuldoj

Tio spegulas la realan laboron de Esperanto-USA kaj samtempe donas al membroj vortprovizon por pli konscie pensi pri propra financadministrado.

Novaj kaj ŝlosilaj vortoj

| Vorto / esprimo (EO) | Traduko (EN) | Klarigo |

|---|---|---|

| ŝuldo | debt | Mono, kiun oni devas repagi al pruntedonanto. |

| kvitigi (ŝuldon) | to pay off, settle | Plene repagi ŝuldon tiel, ke ĝi ne plu restas pagenda. |

| interezprocento | interest rate | Procenta kosto de prunto aŭ rendimento de investo. |

| ĉefsumo | principal | La baza kvanto de ŝuldo aŭ prunto, sen la kalkulita interezo. |

| ŝuldsaldo | outstanding balance | La restanta parto de ŝuldo, kiun ankoraŭ necesas repagi. |

| pagplano | payment / repayment plan | Sisteme aranĝita plano pri kiom kaj kiam oni pagos por redukti ŝuldon. |

| avalanĉa metodo | debt avalanche method | Strategio, laŭ kiu oni direktas pliajn pagojn unue al ŝuldoj kun la plej alta interezprocento. |

| neĝbula metodo | debt snowball method | Strategio, laŭ kiu oni unue kvitigas la plej malgrandan ŝuldsaldon por rapide sperti sukceson. |

| kriz-fonduso | emergency fund | Aparte tenata monrezervo por neplanitaj elspezoj aŭ krizoj. |

| financa sendependeco | financial independence | Stato, en kiu enspezoj kaj rezervoj sufiĉas por kovri bezonojn sen dependi de novaj ŝuldoj. |

Kvankam Esperanto-USA nun ne portas pezajn ŝuldojn, estas grave, ke ni – kiel la estraro kaj kiel membroj – komprenu kiel plej efike uzi ŝuldojn kaj laŭplane kvitigi ilin. Per iloj kiel avalanĉa metodo, neĝbula metodo, pagplano kaj kriz-fonduso, ni povas ŝirmi la organizaĵon kontraŭ estontaj ŝokoj kaj samtempe plifortigi nian kapablon antaŭenigi nian mision.